Trick Question: Do You Want Value or Low Costs?

If you can’t sell all you can produce, then reducing costs is often the only way to improve margins, but that simplistic accounting perspective is not always the case. Cost control is often thought to be key to attaining profitability, but in the case of maintenance it can get you into trouble. Cost control can have a big opportunity cost if you don’t take advantage of the opportunities you have. Consider that what you might really want is greater value – more for less, not just less.

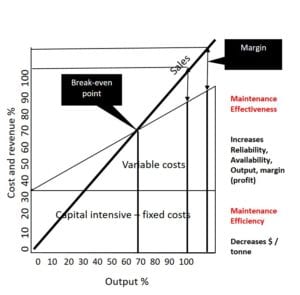

The figure below shows the basics – as production increases, revenues and costs both increase. Revenue is zero at zero production and increases to 100% at 100% output (if you can achieve it).  Fixed costs (e.g., depreciation lease payments, energy to heat offices, someone to answer the phone, etc.) keep the start point for the cost curve above zero. Even maintenance can have some fixed costs – keeping the HVAC systems operational for example. Costs increase as production output increases. Beyond the break-even point revenues eclipse costs and you are making money.

Fixed costs (e.g., depreciation lease payments, energy to heat offices, someone to answer the phone, etc.) keep the start point for the cost curve above zero. Even maintenance can have some fixed costs – keeping the HVAC systems operational for example. Costs increase as production output increases. Beyond the break-even point revenues eclipse costs and you are making money.

Production levels must be kept above break-even in order to generate a margin (earnings before taxes). Margin is represented by the gap between the revenue and cost lines to the right of break-even. As we increase production volumes we also increase margins.

Businesses should maximize earnings. Ideally you produce more, increase revenues (assuming the market will absorb your production) and reduce costs. Cost reduction moves the cost curve down (vertically). Cost reduction may also reduce the slope of the line if variable costs can be reduced. We reduce the slope of the cost line by lowering operating costs. Any cost reduction (fixed or variable) moves the break-even point to the left and increases margins. The gap between revenue and cost lines gets larger.

In the lower cost scenario, the operation produces a profit margin at lower production levels and the size of the gap between revenue and costs increases. Even if production levels remain unchanged, the margin can increase, resulting in substantial improvement in profitability.

Of course markets won’t always absorb more of what you can produce. In those cases you want to produce at lower costs. Consider that increased production levels for shorter times may allow you to shut down for a shift, or a weekend, thus reducing operating costs. Let’s say we can use increased production to either sell more product in a healthy market, or to reduce the number of shifts needed to meet the diminished demands of a tight market. Both are achieved through more reliable operating plant and equipment.

What sort of improvements will help us achieve that? Top-level performers can achieve operating availability well in excess of average performers. So how do we achieve that?

Cost reductions won’t increase output, but they may result from actions taken if output can be increased.

Let’s assume that our maintenance performance has been more or less “average”. Availability and utilization of our assets as well as costs are aligned with industry averages. If we want to be a leader we need to break away from the “average” pack. We will need to focus less on cost and more on reliability. Reliability delivers increased availability for production and, because there are fewer breakdowns, lower costs. The methods used to deliver reliability are also lower cost than those used to repair breakdowns. We need to shift focus from maintenance as a repair shop to reliability.

What sort of benchmark performance do high performers achieve?

Labor utilization (wrench time) increases through better work management practices. You get more work done with the same number or fewer people and manage work backlogs better. Wrench time is up to 52%, not the average of 31%. For that to happen, you must get scheduled work done on time. More work had to be scheduled, it had to be fully planned, materials had to be available and there had to be fewer disruptions from unexpected breakdowns.

High performers do a better job of planning and coordination of material requirements. They don’t schedule without plans nor without knowing that needed repair materials are available. They suffer fewer breakdowns because they are doing more proactive work without over-maintaining. Doing too much of the wrong work can induce failures. They rely more heavily on condition monitoring than preventive work. They know that relatively few failures are a result of aging or usage factors, more are random in nature. All that translates to fewer shutdowns, fewer overhauls, fewer infant mortality failures and overall more availability (uptime).

Choosing the right proactive maintenance approach requires thought about failure modes, their consequences and how they are best managed. The best method for doing that is Reliability-Centered Maintenance. For critical assets you want RCM.

High performers invested in planning, scheduling, materials co-ordination and RCM. They treat these as investments, not costs. Like many lower performers, they probably went through periods of running to failure in a break-then-fix operating mode. They struggled with lack of budget and a lack of cooperation from their operators. They had to find ways to justify the proactive spending.

They had to recognize that you cannot achieve these improvements by focusing only on one thing. Planning, scheduling, materials coordination, PMs and RCM all work inter-dependently for best results – like a meal with many ingredients. Each ingredient provides some benefit on its own, but it is the combination that really delivers the best results. Fixing one alone, like planning, won’t give you big savings. Similarly, don’t believe the hype that RCM is the answer to all your reliability woes. Nor will a new CMMS / EAM system deliver a high return on investment – it actually adds to costs. You need to take a balanced and gradual approach.

What if you are beset with recurring problems from a few machines? A small portion of your assets are causing most of your headaches. Then focus on your worst performers first. Improvements there can pay back quickly and often help fund more improvements. You can usually do this within existing budgets even. If you save on the reactive repairs you can spend more on PMs and the analysis needed to identify which PMs are most effective. You can invest more in planning, scheduling and materials coordination. Gradually you shift from reactive to a more planned, deliberate and proactive approach.

Confidence in your abilities is needed. Without it, you won’t take this risk of reallocating money within your budgets. If you won’t do that, then you probably don’t have what it takes to pull this off. After all, if you don’t believe you can do it, then why should anyone else?

Recognize that you can’t leap to top benchmark performance levels quickly. Target your initial efforts where payback potential is highest. Focus reliability improvement on your worst performers. Plan the most commonly occurring jobs. Don’t fret about spare parts inventory levels or turns. That can come later. The cost of downtime while you wait for deliveries is almost certainly greater than the cost of keeping parts on the shelf. Don’t try to be perfect. Be better tomorrow than you are today and continually improve.

It might take a few years to improve all the way to benchmark levels but all that time you are generating increasingly greater savings and earning potential. An organization that is highly reactive today can expect to take 3 or more years to turn it around. You won’t undo years of poor practices overnight.

At an electric utility we achieved a 34% cost reduction over 8 equipment pilot projects, saving almost $1M a year beginning in the following budget cycle. That took us roughly 6 months from the start of training until the results of those analyses were put into practice. The cost for outside help was roughly $250k over that period. In a large mining operation, we achieved increases of 20% in production over a 6-month period. Revenues in that case were on the order of $100M. The cost of that effort was only $750k! In both cases, waiting for the next budget cycle (and regulatory approvals in the case of the utility) would have been foolish. Cost control in the pure accounting sense wouldn’t have worked, but investing did.

Identify where you have real financial pain that is caused by equipment reliability problems and make those your first targets. You probably don’t embark on major improvement programs all the time – get help from someone who does. Retired help from your own organization is probably the wrong way to get it. No matter how good they may have been at their job, they really only know what you already know. You want new ideas and perspectives – find someone from outside.

Other benefits will also show up in reduced safety incidents, fewer environmental non-compliance events (fines and cleanup costs), and more predictable business results (on-time delivery and meeting targets consistently), less capital investment (the older assets last longer), lower insurance premiums, improved quality performance, improved employee morale and fewer sleepless nights. You probably can’t estimate these up front, but you can track them as you make your changes.

Doing the right maintenance, the right way and at the right time delivers value in many ways. Focusing only on maintenance costs to improve profitability will ultimately get you into trouble and will probably make things worse. Ill-conceived and poorly informed cost reductions often manifest as reduced training, reduced headcount and less proactive maintenance – the only discretionary spending you can really “control”. But smarter managers know that by increasing some of that discretionary spending wisely, will actually generate a reduction in non-discretionary spending on repairs.

Controlling cost in maintenance is not an accounting exercise or the slashing of budgets. Those backfire. Good maintenance cost control begins with a focus on how you can deliver the greatest value through the activities you control. Focus on those that result in reductions in activities you don’t control directly. You can start now, within your current budget constraints, to deliver quick wins and savings. You’ll need to look at planning, scheduling, coordination with your stores, your proactive maintenance program and reliability methods like RCM. It might seem like a lot to do but incrementalism, one method at a time, won’t work well. Hit all those areas gradually but in parallel, going after the “low-hanging fruit” and you’ll find it is doable, even in tough times.